As the British and Plymouth property market navigates the ongoing economic turmoil, many Plymouth homeowners and landlords may feel uncertain about the future.

However, up-to-date data suggests that the 2023 property crash predicted by the many newspapers and the usual clickbait doom-mongers in the lead-up to Christmas on social media, may not be as bad as initially thought, and there are reasons to be cautiously optimistic.

According to property website Rightmove, the average asking price of a home for sale in the UK rose by just £14 in February.

While this might sound like cause for concern, asking prices remaining flat rather than falling could be seen as a positive sign for the year ahead. Remember that they are only what people are asking (and not necessarily achieving).

So, what exactly is happening in the Plymouth property market?

Well, it all starts with realistic pricing.

Thankfully, most Plymouth sellers are heeding their estate agents’ advice and being more realistic on price, helping maintain market stability.

If you are realistic with pricing, the property should sell.

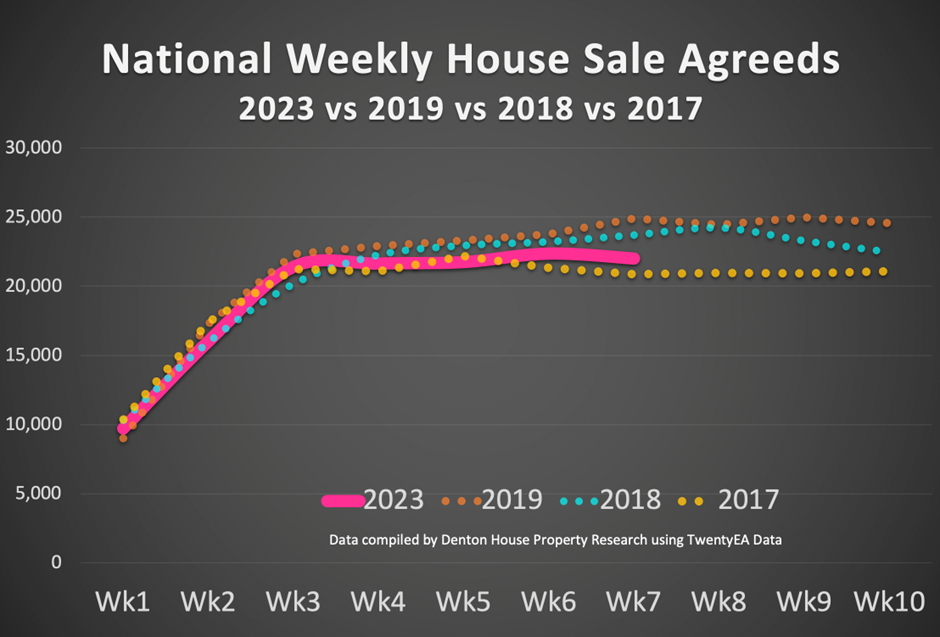

The time it takes to get a property to sale agreed upon has increased nationally from 21 days in the summer of 2022 to around 50 days in Q1 2023.

Additionally, despite the turbulent economic conditions, buyer demand is rising. Rightmove also reported in the national press that the number of people contacting estate agents has increased by 11% in the last two weeks compared to the same period in 2019.

The number of sales agreed upon has also rebounded.

Nationally, from 1st January to the 19th February 2023, 134,886 properties had been sold subject to contract in the UK.

Not a good figure when I compare it with the same year-to-date sale agreed figures from the last couple of years.

2022 – 173,607 properties sold stc

2021 – 193,607 properties sold stc

But the last couple of years have been extraordinary for the UK property market and should be taken with a pinch of salt in some respect. We must compare 2023 with more normal years, like 2017/18/19/20. This tells a different story.

2020 – 151,694 properties sold stc

2019 – 143,504 properties sold stc

2018 – 138,665 properties sold stc

2017 – 134,503 properties sold stc

The picture looks similar when we look closer to home in Plymouth.

In Plymouth (PL1 to PL9), in the first seven weeks up to the 19th February 2022, 835 properties sold subject to contract.

This year, from the exact 1st January to the 19th February timeline, 721 properties have sold stc, which is lower, yet in the same ballpark as 2017, 2018 and 2019.

Yet it is all terrific selling a house (subject to contract); it is still only sold subject to contract, meaning the sale could fall through (as it is not legally binding).

As an agent who likes to delve deeper into statistics, I considered the ‘net property sales’. (Net Property Sales being the gross number of properties sold that week less the sale fall throughs in the same week).

In the three months leading up to the Mini-Budget in September 2022, there was an average of 17,801 ‘net property sales’ per week in the UK. That dropped by 34.7% two months after the Autumn Mini-Budget to an average of 11,624 ‘net property sales’ per week in the UK.

In the last five weeks, that has rebounded to 17,050‘net property sales’ per week.

And when you consider the average for the same five weeks in 2017/18/19 was 18,330 ‘net property sales’ per week, we are close to what many considered a normal market.

Improving market conditions has been supported by a reduction in average mortgage rates. Homebuyers taking out a five-year fixed-rate mortgage with a 15% deposit can expect a rate of 4.39% (correct at the time of writing with HSBC), down from an average of 6.1% in early October. This reduction in mortgage rates may have contributed to the recent increase in buyer demand.

These positive signs in the market have led some experts to suggest that a ‘softer landing’ for the UK property market than initially expected could be on the horizon.

The combination of sellers being more realistic on price and an improving picture of the number of agreed-upon sales suggests a more positive outlook for the property market.

I advise Plymouth homeowners coming to market in the upcoming spring season to use their agent’s expertise and get the price right the first time to find the right buyer more quickly. If you do wish to chance a higher asking price, only do so for no more than two weeks. If you haven’t sold by then, take the agent’s advice and realign your asking price.

477 Plymouth homeowners have realigned their asking prices since 1st January 2023.

While it’s true that some first-time buyers may still be priced out of their original plans and may need to look for a cheaper property, save a bigger deposit, or factor higher monthly mortgage repayments into their budgets, there is still cause for optimism.

There is still a considerable demand for buying property in Plymouth – renting is becoming increasingly unattractive for many people as rents are increasing by double digits percentages.

It is important to remember that purchasing a property always involves a trade-off between what one desires and what is affordable, regardless of the market conditions. For example, while a four-bed detached house may be out of reach, a larger and older three-bed semi-detached property may be a more realistic option (and probably have similar square footage).

Plymouth landlords looking to invest in buy-to-let homes – now may be a good time, as rising rents could offer attractive returns.

Of the 545 properties let in Plymouth since the 1st January 2023, the average rent achieved has been £827 per month. This is a significant drop in the number of properties let in the same first seven weeks of the years of 2017/18/19 and a massive increase in rents.

Finally, the newspapers will be full of news about house price drops in the coming months. All the indexes report house sales where the sale agreed price was offered nine to eleven months ago and completed (i.e., monies and keys handed over) three or four months ago. This peculiar time lag means the house price data is nearly a year old before publication.

So, if you decide to buy a home on that information, you are using old property data. In late 2021/early 2022, there were 30+ viewings per property, and people paid way over the asking price to secure a property. Now there is more ‘normality’ in the Plymouth housing market; today’s prices are also more normal (at or slightly below the realistic asking price). So yes, the house price indexes will show a reduction in house prices. The newspapers will say house prices are crashing, yet when it is explained I have above … whilst it is not a newspaper clickbait title – it is the truth and it’s more of a return to more ‘normal house prices’.

So, prepare for clickbait newspaper headlines of a house price crash (because ‘bad news sells newspapers’ as the saying goes).

Also, prepare for the doom-mongers to quote the bad news of the earnings-to-house prices ratio at one of its highest levels ever.

Earnings-to-house price ratios are a poor measurement of health in the UK property market. Instead, I believe Nationwide’s measure of first-time buyer mortgage payments as a percentage of take-home pay is better (as it is actual pound notes out of actual pay packets).

The Nationwide measure of first-time buyer mortgage payments as a percentage of take-home pay has grown for first-time buyers from 30.4% in Q4 2021 to 39.4% in Q4 2022 … a massive rise! Yet mortgage interest rates have dropped since then (so that percentage will fall). Also, to give some context, let us not forget that percentage in 1989 was 48.4%.

Ultimately, Plymouth homeowners and landlords should decide, based on their unique circumstances, rather than being swayed by newspaper headlines or general market trends. Anyone uncertain about the property market’s future should contact me for my opinion, advice and guidance.